Placement of Deposits by UCBs

In recent years, the Reserve Bank of India (RBI) has heightened its scrutiny of cooperative banks, leading to penalties being imposed for violations of prudential norms. The breach of these norms stands out as a significant cause for such penalties among UCBs. In 2023, approximately 35 UCBs (as per data compiled by Annuity Risk) were penalized for failing to meet prudential limits, while in 2022, about 30 UCBs faced similar penalties. This heightened regulatory attention emphasizes the critical need for stringent adherence to RBI guidelines to avoid penalties and uphold the stability and integrity of the banking system.

In 2001, the RBI first addressed the issue of Urban Cooperative Banks (UCBs) holding deposits or funds with another UCB. At that time, the concern revolved around the potential systemic risk posed by UCBs and how it could be transferred to the bank holding the funds. Consequently, the RBI prohibited UCBs from depositing their funds in other institutions or public sector companies.

In 2003, this regulation was revised to permit a few strong scheduled UCBs, complying with specific norms, to accept deposits from other non-scheduled UCBs. This framework remained intact, and in 2015, stricter norms were implemented to qualify a scheduled UCB to accept deposits from non-scheduled UCBs.

The criteria for qualification as ‘strong scheduled UCBs’ according to the 2015 RBI guidelines for Placement of Deposits with Other Banks by Primary (Urban) Co-operative Banks (UCBs) are as follows:

- Maintaining a Capital to Risk (Weighted) Assets Ratio (CRAR) of 10% or higher.

- Keeping Gross Non-Performing Assets (NPAs) below 7% and Net NPAs not exceeding 3%.

- Ensuring a record of net profits in at least three of the previous four years, provided there is no net loss in the most recent year.

- Adhering to Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements.

- Ensuring that net NPAs do not exceed 3%.

- Implementing a robust internal control system with a minimum of two professional directors on the board.

- Fully implementing Core Banking Solution (CBS).

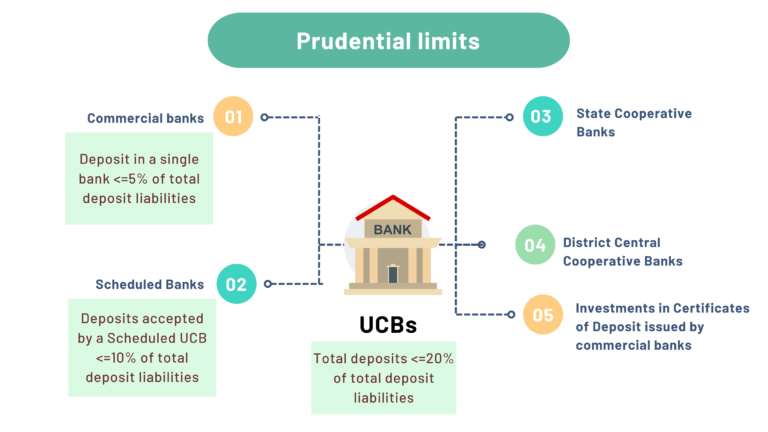

| Prudential Limits | % if total deposit liabilities |

|---|---|

| Prudential inter-bank (gross) exposure limit | <= 20% |

| Prudential inter-bank counterparty limit | <= 5% |

| Total inter-UCB deposits accepted by an eligible Scheduled UCB | <=10% |

One of the primary challenges faced by cooperative banks is monitoring and complying with the complex web of prudential norms set forth by the RBI. Failure to comply with these norms not only exposes banks to regulatory penalties but also causes a loss of reputation and public confidence in an otherwise healthy bank. The penalty is decided by RBI under the provisions of Section 47A(1)(c) read with Sections 46(4)(i) and 56 of the Banking Regulation Act, 1949. The maximum penalty amount specified is “one crore rupees” or twice the amount involved in the contravention or default, whichever is higher and quantifiable. If they continue to exceed the limits additional fees may apply. A further fine, not exceeding “one lakh rupees” for every day during which the contravention or default persists, can be imposed. For a young UCB with a balance sheet of INR 100 crores and net income of 1 crore, such substantial fines can have catastrophic consequences. Currently, there are 715 such UCBs with balance sheets totaling less than INR 100 crores¹.

To navigate these challenges effectively, cooperative banks must leverage advanced compliance software solutions tailored to the specific requirements of the Indian banking sector. Here’s how such software can be instrumental in ensuring adherence to RBI’s prudential limits:

Automated Compliance: A robust software automates monitoring of key parameters like CRAR, NPAs, inter-bank exposure, and deposit acceptance limits. This enables prompt identification of regulatory deviations and proactive rectification.

Real-time Reporting: The software offers real-time reporting, ensuring accurate and timely compliance status updates. This enhances transparency and accountability, aiding decision-making for both management and regulators.

Risk Assessment: Advanced algorithms evaluate the financial and reputational risks of non-compliance, aiding in prioritizing remedial actions and resource allocation effectively.

Custom Alerts: Tailored alerts notify stakeholders of any deviations from prudential limits, enabling swift corrective actions and preventing escalation.

Seamless Integration: Integration with existing banking systems, such as CBS, streamlines compliance monitoring, offering a comprehensive view of compliance status and facilitating informed decision-making.

In conclusion, investing in a robust compliance software solution is imperative for cooperative banks and UCBs seeking to uphold RBI’s prudential norms and avoid regulatory penalties. By leveraging advanced technology to automate monitoring, enhance reporting capabilities, assess risks, and enable proactive compliance management, banks can strengthen their regulatory compliance framework and safeguard the stability and resilience of the banking sector.